The news that Coursera has raised a US$130M Series F round, valuing the company at a reported US$2.5B, caught my interest. If I could invest in one late-stage edtech company, Coursera would be it. There is a global need for lifelong learning; and the company is well-placed to meet it.

Background: the demand for online lifelong learning

Given that a large percentage of the population in developed countries already has a bachelor’s degree, my starting premise is that there are two main sources of growth left for higher education: first, people in newly affluent emerging markets, who can afford access to higher education for the first time; and second, lifelong learners, particularly in developed countries. (For more detail, I recommend Studyportals’ 2018 report, “Envisioning Pathways to 2030: Megatrends shaping the future of global higher education and international student mobility”, available here.)

The second opportunity is the key. While recent events have shown the limitations of attempting to deliver undergraduate (and K-12) education online, online education is much better suited for working adults who already have their first degree. These individuals are motivated; already have study habits; and need the additional flexibility that online delivery provides. This can be seen in data from the US, where over 30% of post-baccalaureate degrees are done wholly online (and a further 9% included an online component).

For corroboration, we can look at listed public companies that operate in the online program management (OPM) sector, which helps universities launch online degrees (typically at master’s level). These include 2U, as well as the respective arms of Pearson and Wiley. All three post organic revenue growth in the 10%-15% range year-on-year. (While 2U’s headline revenue growth rate is typically higher, this tends to reflect M&A.)

Enter Coursera

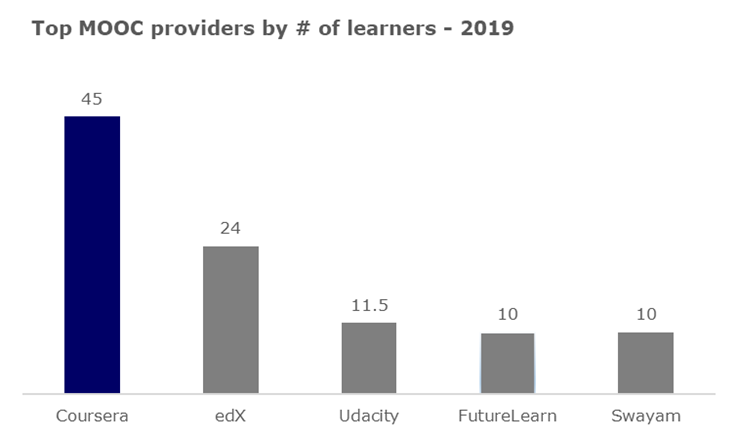

This is where Coursera, and its peers, come in. Established in 2012, Coursera helped pioneer Massive Online Open Courses (MOOCs) – short, university-branded courses that the company offers through its portal. Today, it is the world’s largest MOOC provider, with 45 million registered users as of 2019 — this is over 40% of the worldwide total, excluding China.

Coursera’s course offering spans the range from individual MOOCs up to full degrees. The following figures are from Coursera’s “About” page, as of July 2020:

- 4,500+ courses from university partners on a freemium model;

- 450+ micro-credentials comprising a linked series of courses, some of which bear university credit;

- 30+ certifications from corporates such as Google and Amazon (AWS);

- Fully fledged degrees from its university partners, including marquee institutions such as the University of Pennsylvania and Imperial College London.

Growth has been significant. While the company has not disclosed its revenue, Forbes estimates it grew from US$140M in 2018 to US$225 million in 2019, and forecasts another 30%-50% growth in 2020. The pandemic has led to another surge in interest — the company’s CEO telling Forbes that enrollments “quintupled” YoY — although we do not know the extent to which this will translate into an increase in paying learners.

An advantageous model

There is significant competition for these opportunities. Coursera competes against OPMs; against online providers offering their own proprietary content, such as Udacity and coding bootcamps; and against other MOOC providers that offer both short courses and full degrees, such as edX and FutureLearn. Nonetheless, I consider it well-positioned.

A large part of my argument is that, as a MOOC provider, I consider Coursera’s business model better than many competitors. Unlike an OPM, it has a consumer-facing brand: I can and do browse Coursera’s catalogue, looking for interesting courses. And it can build that brand by providing free courses, such as a recent, COVID-era program granting access to university students for the next few months. My hypothesis is that this should pay off in lower student acquisition costs vis-a-vis the traditional OPM sector, which traditionally incurs extremely high marketing expenses — 50%+ of revenue for 2U.

Meanwhile, I see university relationships and university-provided courses as an advantage. Relative to providers of proprietary courses, I think it is easier for universities to differentiate. Universities abound in expertise, both in breadth and depth. Their reputations stretch back decades — in some cases, centuries. A course from Harvard or MIT stands out; whereas it can be very hard to tell the difference between coding bootcamps.

Finally, I think there is a virtuous, self-reinforcing cycle here. The more university partners — especially highly ranked university partners — and courses there are, the more attractive Coursera is to students. And the more attractive it is, the more likely students are to visit its site, and perhaps sign up for a course or two.

First among equals

While edX and FutureLearn enjoy these same advantages, I expect Coursera to remain significantly larger. Even after COVID increased website traffic for all the major MOOC providers, Coursera remained ahead. As the largest MOOC provider, I expect Coursera is front of mind for learners — students presumably think of, and visit, coursera.org before edx.org or futurelearn.com.

I should stress that I don’t see this as winner-take all, and I certainly don’t expect Coursera to drive the others out of existence. EdX has a track record of interesting initiatives such as MicroMasters (microcredentials that bear cheap credit at Master’s degree level), and now MicroBachelors supported by student success coaches (student success and retention have historically been a stumbling block for online education). FutureLearn has carved out a niche in the UK and Commonwealth. They have excellent content — there is a Japanese history MOOC on edX that I really want to finish! But I do not expect them to dethrone Coursera in the foreseeable future.

Valuation: how does it compare?

As much as I like the company, valuation forms a critical part of any investment process. Can we compare the current round (US$2.5 billion) to an estimate of fair value?

In this case, the data is spotty; we do not have enough information to attempt a DCF valuation; valuing high-growth companies is always more of an art than a science; and that imprecision goes doubly so for venture rounds. Nonetheless, we can try using the one metric we have: revenue.

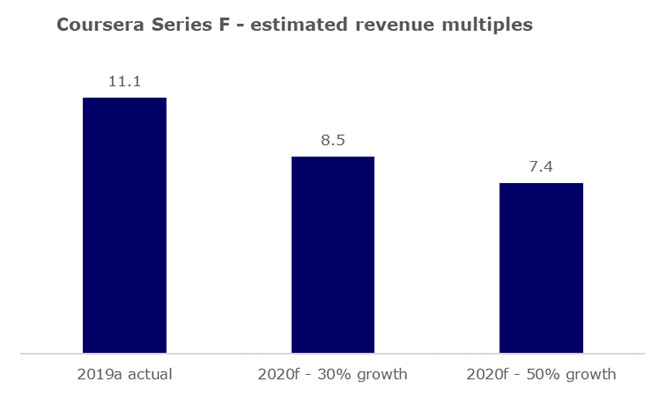

Going by Forbes’ estimates, 2019 revenue was US$225M, and assuming 30%-50% revenue growth in 2020, revenue would be between US$293M and US$338M. This suggests a multiple of 11x trailing revenue, or high single-digit forecast revenue:

Now we can compare this to the following data points:

- Historically, OPMs have tended to transact on revenue multiples in the mid-single digits (e.g. Grand Canyon/Orbis, at slightly under 6x revenue).

- The closest there is to a pure-play listed OPM, 2U, trades on a low single-digit revenue multiple (but this was after sharply disappointing the market last year).

- Instructure, the developer of the Canvas learning management system, was recently acquired by Thoma Bravo for approximately 6-7 times revenue.

- Pre-COVID, SaaS businesses tended to trade on anywhere from mid-single digits up to 20x revenue multiples, depending on growth rate and margins.

- M&A transactions need to be adjusted to reflect control premia.

If we compare the multiples corresponding to Forbes’ anticipated revenue growth (around 7x to 9x), the latest round would price Coursera at a premium to edtech M&A (Instructure and OPMs); and within the range more typically associated with SaaS companies. Worth it for a market leader? Time will tell.

Conclusions

Coursera is a company I have watched for a very long time, first as a learner — I have fond memories of history courses taken in the site’s early days — and then professionally. Media interest has come and gone; but Coursera (along with its peers) has added content, course types, and users. It appears to be paying off, and I look forward to seeing how the company evolves.